I’ve been posting about this since last summer, when I started noticing some disturbing trends. First, the stock market valuations are way off. The current P/E ratio of 28.77 is significantly higher than the historical average of 18-19.

More importantly, the distribution of market share is less than it has ever been. Together , “Magnificent 7” stocks have an astounding 33% share of the S&P 500. These 7 tech giants have a combined $16 TRILLION in market value. That is, in my opinion, way too few stocks to hold such a vast market share.

This phenomenon leads to concentration risk, which means that too few stocks account for such high valuations , especially since they’re in the SAME industry instead of a diverse group of industries, which makes the entire market more vulnerable to an economic crisis.

We will get a closer look at this in the coming week, when NVIDIA reports earnings. $NVDA results can swing the entire market wildly in either direction, despite accounting for less than 1% of the nation’s economy.

A FRAGILE SITUATION…

So whether the economic pain comes sooner or later rests with several factors, such as macroeconomic conditions, employment, the health of the banking system, and the speed of negative economic impact from President Trump’s policies. But the biggest factor of them all, general market sentiment, is contingent upon all of these. And, this can be impacted significantly by the moves of a single stock.

MSFT, GOOGL, AMZN, AAPL, NVDA, META, and TESLA make up 33% of the S&P 500

We are currently in our 2nd year of substantial inflation, just as we’ve been predicting since 2018 (the pandemic stalled the inevitable), and as our last blog post spelled out, policy makers are terrified.

Although there has been some easing in prices (mostly energy) consumers have not stopped spending, and housing shortages are causing the overall cost of living to rise.

So we were right in saying that the Fed is willing to wreck the economy over its’ fear of inflation. High inflation only gets worse if it’s allowed to continue. Here’s what Jerome Powell said in his latest remarks;

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses,” he said in prepared remarks. “These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

The best people can do for themselves right now is 1. Avoid taking on any new unnecessary debt. 2. Cut up your credit cards and 3. reduce expenses.

After having predicted strong inflation far before most world-renowned economists, and after being similarly ahead of most others in instantly swatting down Jerome Powell and Janet Yellen’s views that inflation was transitory, we’re going to take a deep dive into what’s steering the US economy right now, and more importantly, where it’s going.

With the latest US inflation data in and running at a white-hot 8.6%, the answer to the question is a strong YES, as the Federal Reserve will be frightened into beaching the giant ship that is the US economy. Runaway inflation is a deep and valid concern, and interest rates is only one way to try and tackle the problem. The other ways to tackle the problem largely depend on consumer behavior, which will inevitably take a hit due to the cascade of bad news coming out about the economy.

Prior to the inflation announcement today, there was some hope that the Fed could “thread the needle” and escape a recession. Even here at REconomixTM we were slightly hopeful of such a scenario. Now that inflation has become very entrenched, the Fed must try its best to slow down the economy.

Structural Problems

As we all know, the Fed “printed” money for more then a decade, and the supply of money grew so large, it created asset bubbles. This is because in capitalism, money likes to go where it’s “taken care of,” and it likes higher returns. The result was asset bubbles in stocks, real estate, and cryptocurrencies, amongst others, which are being deflated by the promise of ever higher returns in safer assets, along with the slowing of demand in loans from banks. People tend to take out smaller loans, or none at all, when the cost to pay them back goes up.

The US economy is very exposed to the rest of the world because of the amount of free trade deals, exports, imports, and the amount of multinational corporations bringing profits or losses back home. The post-pandemic world saw a stimulus from central banks around the world, which means that money supplies increased, ultimately causing consumers around the globe to purchase more goods and services.

India and China are massive economies with growth trajectories which cause a rise in consumption of food, and other commodities around the world. In fact, if it weren’t for the state-mandated lockdowns in China, the global inflation problem would actually be worse!

Fiscal Policy

In the past 2 decades, the US government, as the “spender of last resort,” has propped up the flagging economy through running large budget deficits. This started with the Bush administration post 9/11, and increased during the Obama, Trump, and now Biden administrations. Much of the spending has been focused on defense and national security. In the course of the last 2 decades, defense and homeland security spending has been profligate at times. As one example, an entire fleet of new ships, called Littoral class destroyers, was created at a cost of several billion dollars. They are now rendered impractical and vulnerable, and are slated to be scrapped or sold off.

Energy

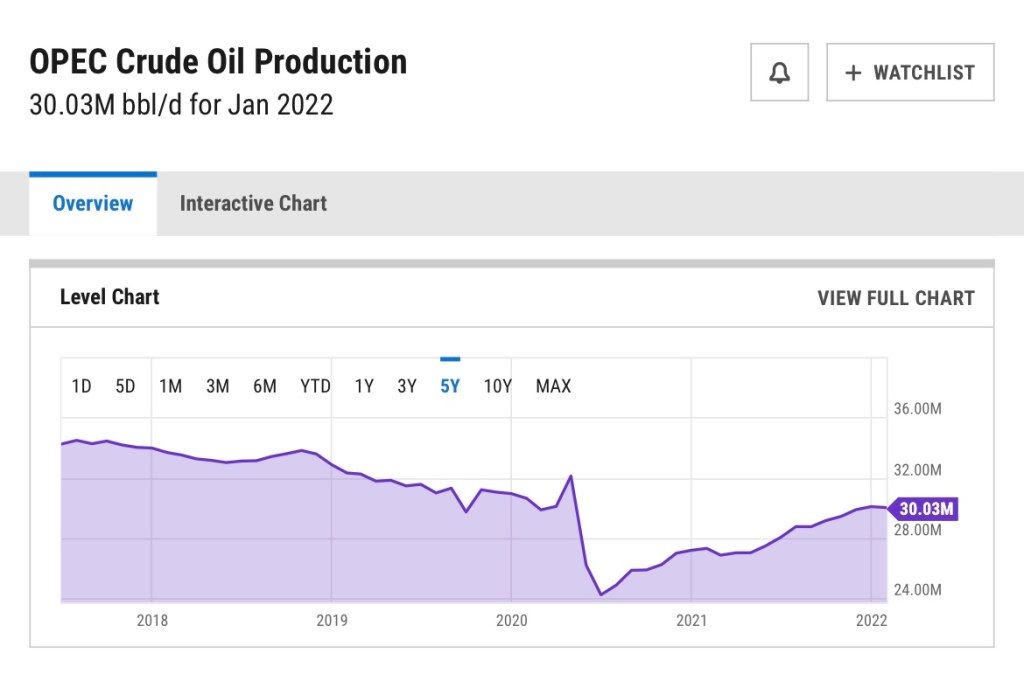

During the pandemic, the price to drill and transport oil got so low, it cost more to ship it and drill for it than it was worth. The demand for oil was extremely low compared to the supply. Large oil-producing countries, especially OPEC, decided that they would put limits on the production of oil to try to boost the price. Since the boom in global demand from people getting back to work, those production cuts are still in place.

Russia’s invasion of Ukraine resulted in sanctions of Russian oil and gas, which removed millions of barrels of oil a day at a time when we needed it most. To date, OPEC has not made any meaningful production increases to offset Russian oil. OPEC seems to be cashing in and making up for any losses from the pandemic.

Even as demand has increased, OPEC oil production is well below 2018 levels. Source: ycharts

Food

Food is a core necessity, like energy, and the prices of food are affected by energy. It takes energy to produce food products, refrigerate them, and transport them to stores. Agriculture has been affected by the rise in trade and incomes in China, as well as 3rd world countries, notably India, Africa, the middle east, Central and South America, and southeast Asia. As incomes rise, people tend to consume more food, and unfortunately, waste more food.

The price of wheat has doubled in the last year, especially since the war in Ukraine started. Source: CNBC

Other commodities

As the world increases in affluence and wealth, (especially India and China, which combined, have 2/5 of the world’s total population) commodities become more scarce during economic expansions. This includes metals, precious metals, and other goods.

Supply Chain Breakdowns

Post-pandemic, the supply chain disruptions were rightfully blamed for much of the rise in prices due to spot shortages of goods and commodities. It was relatively easy to return to work in the service sector, but the manufacturing and shipment of goods and commodities was greatly affected. This will be less of a factor over time, but many shortages remain.

The Perfect Storm

In conclusion, the aforementioned factors, and others have created a perfect storm of uncertainty, scarcity, war, fiscal irresponsibility, and irrational exuberance. The coming recession must be handled carefully by those in charge, as to not cause panic or severe disruptions and further scarcity in necessities. If the past is any indication, we are headed for political upheaval and widespread dissatisfaction with the status quo.

I’ve been predicting higher than expected inflation for years. Then, as soon as Fed chairman Jerome Powell told the world that an unexpected level of “transitory” inflation was here, I told you it wasn’t transitory. Turns out I was right on that one too. So how does one humble student of the global economy and finance beat the consensus of an entire Federal Reserve Board of Governors and their army of researchers ??

Inflation is not a only a US problem, but a global problem post-pandemic.

For one thing, I live in reality. Also, i’ve been watching the economy, the Fed and government long enough to block out all of the noise. I don’t know what goes on in the minds of the Federal Reserve Board, but I know that most of what we see and hear in the business, finance and economic world is pure noise. Behind nearly every click-bait headline is either a hidden agenda, a skewed worldview, a political axe to grind, or a school of economic thought to defend.

That said, I’m not some wonky, data-mining, hyper-intensive researcher, either. I’m just a guy who has several invaluable assets. Among them, common sense, a comprehensive knowledge of how the global financial systemreally works, and several tenets I adhere to when dissecting and interpreting data.

US Government fiscal policy, not just Fed policy, is a major driver of inflation.

Now, predictably, the financial and economic world is highly critical of, and scrutinizing every move by the Fed, and will undoubtedly overreact to every announcement. This is foolish. Fed policy isn’t the only game in town. There’s also fiscal policy, consumer behavior and sentiment, and the ever-present threat of game-changing world events (see Covid-19).

These other factors have even more of an impact than the Fed does on the economy at any given time, but it was the decade-long and unprecedented intervention of the Fed coupled with out-of-control fiscal policy that led us to these high levels of inflation. Add in the effects of the pandemic and global supply chain disruptions, and you have a perfect storm for what is happening. Could it have been avoided? Absolutely. But that is for another blog post.

With everyone now second-guessing the Fed (eerily reminiscent of 2008), including former President Trump’s attacks on Jerome Powell in 2019, the tail is now wagging the dog. Wall Street hedge fund manager Bill Ackman rightly tweeted yesterday that the Fed should come out with a large interest rate hike out of the gate. I couldn’t agree more. But with both the Fed and President Biden caught off-guard and leading from behind on this issue, the result is pandemonium. The panicked armchair quarterbacking from across the economic and political spectrum will not cease.

Expect the “independent” Fed to be reigned in

Say hello to new levels of grilling by Senate committee members for their own political posturing. Say hello to political pundits, wall street loudmouths, celebrity billionaires and former heads of so-and-so *cough Larry Summers cough* saying how they would have done it better.

Almost certainly, none of them would have done better than Jerome Powell. This is because the Fed is run by a bunch of bankers. Those bankers know how to make money for only one group of people exceedingly well. Fellow bankers. Although the Fed has a dual mandate, “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” they’ve shown a strong inclination toward doing what wall street and the financial/economic elite tell it to do.

After this, those same actors will have an even louder voice and influence on the Fed, ending whatever independence the Fed was supposed to have in the first place.Thus, ending the Fed as we know it for the foreseeable future.

As usual, my busy life keeps me from posting blogs about the economy, but no more excuses!

Inflation was being baked-in to the economy well before the pandemic started.

A few of us have been warning people for years about inflation . Not just the occasional tweet of concern, but actually screaming about it via text, and even getting into twitter arguments with people who were absolutely certain that I was wrong.

So ok, now what? Predicting things can be easy sometimes, but what comes next is usually tricky. Not this time. What comes next is entirely predictable.

The first question we must ask ourselves, is whether this inflation is “transitory” as the rudderless Federal Reserve tells us, or whether it’s longer-term, or even, dare I say, structural.

The answer to that is easy for someone like me, because I’ve been watching it build for awhile now. It’s obviously been baked-in to the economy over time- so it is, in fact, long-term.

The Fed has based the monetary policy of the largest economy in the world on a deeply flawed model.

Why isn’t it transitory? That has been ruled out, because many of us who predicted inflation did so well before the pandemic started. The Fed tells us it’s transitory because of a post-pandemic rise in consumerism, and the economy getting back to work. This belies the underlying cause of the inflation itself. The pandemic slowed things to a crawl, and put a temporary hold on inflation. The government, along with the Fed overcompensated (as they often do) and printed trillions of dollars in new cash to break us free from the economic doldrums, and here we are.

Why isn’t it structural? This, because the Fed has lowered interest rates to near zero, the Fed has a lot of medicine to combat inflation. They can also stop printing money. However, it can be bitter medicine, and the delusional Fed has refused to use it, because it would slow down the economy. Slowing down the economy is never a popular idea.

Screaming into the void.

Can inflation become structural? It can, because if the Fed and the US government don’t pull back support quickly, inflation can become runaway train. Inflation breeds inflation, and the worst kind can be programmed psychologically into the consumer. Pulling support from the economy will also have consequences, but it is the bitter medicine we must take.

When a consumer senses something will go up in price if they don’t buy it now, that creates a ripple effect on the economy for necessary goods. This translates into shortages of those goods, and people stop buying unnecessary goods, slowing other parts of the economy and creating a vicious cycle of economic damage and inflation at the same time. This scenario can be down-right frightening.

How can we stop this? Who needs to “step up”? How much time do we have? These topics will be covered in coming blog posts, since this one has gone on a little long.

The United States economy is often compared to an aircraft carrier by experts. It’s massive, and is steered very slowly. Much like an aircraft carrier, it also has millions of moving parts. Some of those parts are human capital, while others are systems and machinery, much like American factories, supply chains, pipelines, and so forth. So when we’re talking about an entire economy in an article or blog post, it’s incredibly easy to leave out thousands of minute details that make the entire machine work.

However, you can take some solace in the fact that much of this giant economy is run by experts.

Yes I said it, but it’s likely not what you think.

Those “experts” are not at the top sometimes, but rather somewhere in the bottom of the ship, running the thousands of moving parts. American workers can extract minerals and resources from the ground, and grow food to feed the population. American engineers can turn those raw materials into useful everyday products, and factories can run the machinery to manufacture those products. American transportation experts and workers can move those goods to retailers, restaurants, grocers, and distribution hubs. American tech companies know how to provide the technology and support for these massive endeavors, and so on.

So, regardless of the Fed moves that are mucking things up, human capital knows how to make adjustments and decisions on the fly, in order to position themselves and their tiny individual sections of the economy for success. We saw this happen all through the pandemic, when millions of families and small businesses made tough decisions everyday in order to survive. Now, with the pandemic at least partially behind us, we must commit ourselves to the hard work of making this giant ship move out of the dire straits we’ve encountered along the way.

I’m kicking myself for not posting this yesterday, like I wanted to. Today, with the Dow down around 800 points and NASDAQ down around 600, I may seem like I’m being captain obvious.

However, with the NASDAQ only down 3% and the NASDAQ only down 4.5% off of record highs, I believe that gravity will not let up so easily.

Sure, some Robinhood investors may see this as a chance to catch some stocks on the cheap, but we’re talking fundamentals here! Most of the people on Robinhood don’t know a thing about market fundamentals, and those who do will likely scoff at the very subject.

Back in the year 2000, while I was taking an Information Technology class in college (more specifically -Oracle), I recall one student loudly telling another that his JDS Uniphase stock had nearly doubled to something like $105 per share. The Dot-Com bust spared almost no tech company, including the biggest names in tech at the time.

A year later, JDS Uniphase was clinging to $5 a share. Yes, the stock recovered much later, but the moral of the story is simply keep your powder dry. There will be a chance in the future to make money in the market. Now is not the time. Park your cash in different places, earn that measly percentage rate that your family & friends are joking about, and wait patiently.

INFLATION

One of the main caveats to holding cash is inflation. But with 30 million people out of work, stores and small businesses closing by the thousands, and millions facing eviction, that’s not a worry right now.

Yes, the Fed will likely print more money, but it’s extremely likely that will be eaten up feeding liquidity into a the market in any kind of event like the one we see today. That, my friends, will largely end up in the pockets of a handful of billionaires and opportunistic investors (kinda like us, but with more access) who will be buying real estate, equites and other assets at a very nice discount.

An article recently stated that many people are googling “should I buy a house?” They are concerned about the economic impacts of COVID-19 but want to take advantage of historically low interest rates.

Buying a house is a very long-term decision. Although we have no idea how long this pandemic will be with us, note that past pandemics have been relatively short-lived.

If you are financially stable, can afford it, don’t fear a loss of your job, and you see a good opportunity, take it. You will look back on it many years later as a wise decision. But don’t just buy a given property based on low interest rates. Rates will likely stay low for the foreseeable future.

Don’t try to time the market either. If you believe sales may tank and housing prices will go down, you may want to wait, but remember, housing supply is still low, so when demand eventually does come back, housing prices will go up with it. Moreover, If the pandemic ends relatively soon, you could see most prices stay right where they’re at.

Several people have asked me if they should liquidate their 401k. The short answer is no, wait things out. I will discuss this in more detail in a later post. Don’t forget there are taxes, and also penalties for pulling funds too early.

That said, if you are really business savvy you can invest the funds in real estate or even purchase a small business that has good financials and a proven track record. Both can be very risky, please do your research and don’t take anyone’s word for it, make sure a licensed CPA certifies the company’s financial statements before buying, and use an escrow account. Please consult with licensed experts such as a contract attorney before signing any paperwork!

Quietly and calmly go to your nearest bank or credit union and pull some extra cash out. The banking system took a huge hit today and it took a $1 Trillion injection of cash in order to shore it up. It kept markets running, but didn’t help investor confidence. Another big hit, and markets can panic even worse, making these injections useless. Banks may have short-term liquidity problems, meaning that they won’t have enough cash on hand in an event that people start running to their banks to pull out cash. At that point, even ATM card readers may be unable to process transactions in some instances, and CASH WILL BE KING , especially when you need it for food, water or an emergency.