Saturday, May 3, 2025

Here, I give a “plain English” explanation and some direction as to where we’re headed economically speaking. After predicting massive inflation, slapping down the “transitory” label that the Fed famously fumbled, predicting numerous small corrections and the Big correction this year, I’ve been on a nonstop win streak since at least 2015. Predicting major macroeconomic moves is part science, art, psychology, and patience, but mostly, you must learn and constantly reinforce your knowledge about what moves markets and economies. There are indicators, some sophisticated, some very simple. There are fiscal and political aspects, monetary aspects, consumer habits, commodity supply and demand, etc. But one of the most important things, is that you must understand these things in relation to one another, their relevance, and have a clear mathematical perspective, so that you know which data to disregard, or apply less “weight” to. Numerous business articles are published each day. Some may be important to certain sectors and industries, but mostly, they are not important to the macro economy.

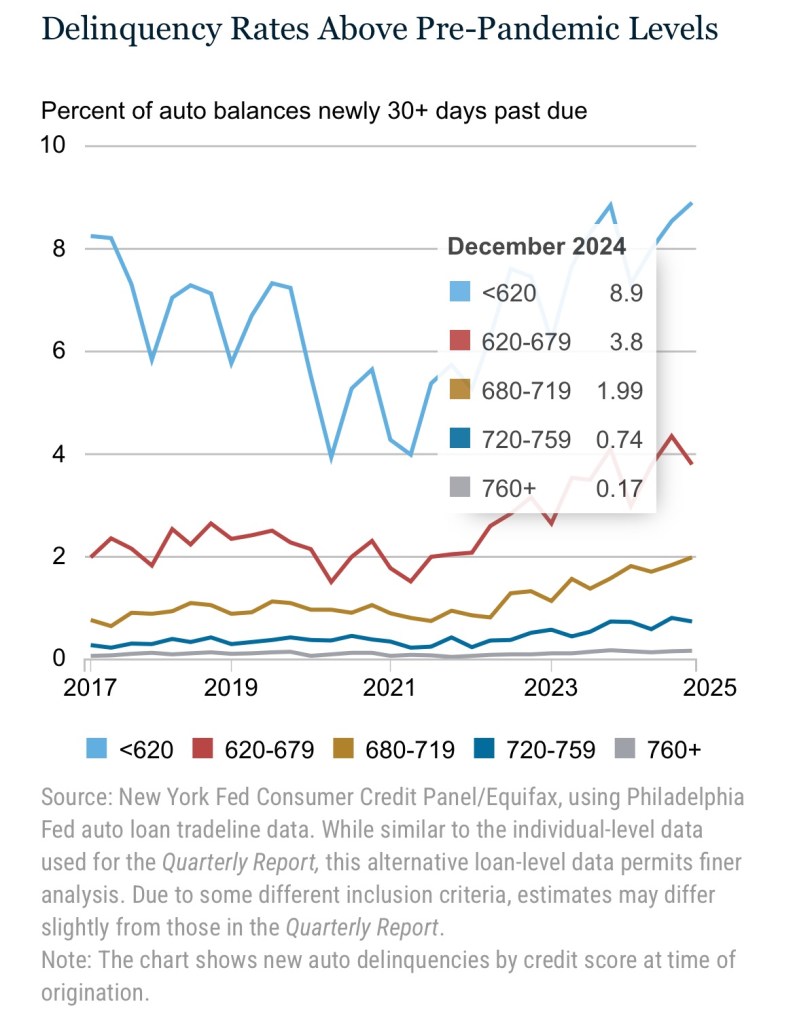

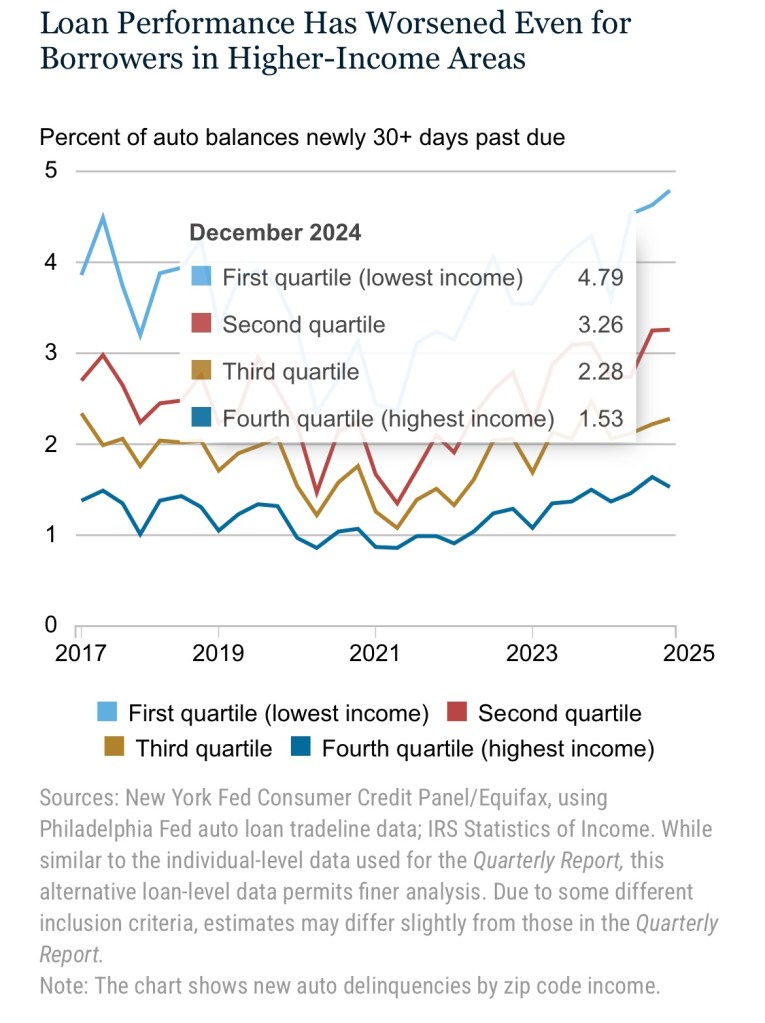

Speaking of indicators, we have a big group of indicators screaming at us! There is underlying weakness in the economy that the markets haven’t reacted to, because it’s too wrapped up in the 24hr news cycle. But the market psychology of the 24 hr news cycle is a whole topic for another discussion. Here are a few screaming indicators:

We also have some major issues at the forefront:

- Trade/ Tariff negotiations. These aren’t going as well as hoped by the Trump administration. There will be some “big” (read: amplified) announcements, and they will try to put the best light on them, but the whole thing, short of rolling them back almost completely, is a debacle. It was botched from the beginning, and they will mostly have both short (inflationary) and long (industry altering, layoffs) effects on the economy.

- Interest Rates. The most obvious example of the economic illiteracy and ineptitude of the current administration was back in April, when Mr. Trump tried to pressure Fed Chairman Powell into lowering interest rates. The bond market, the true masters of the financial world, slapped him down. Then, he tried to get Powell fired and again, the bond market said no. Time for a quick note on the Fed and its chairman; first, the Fed is run by bankers. Yes, there are economists on the board of governors, but mostly to advise bankers, as they do on Wall Street. Big banks decide who the Fed governors are and who the chairman is. Period. If the Masters of The Universe- people like Jamie Dimon, Larry Fink, Steven Cohen, etc. decide they don’t like the Fed Chairman, rest assured, he will be gone by way of pressure on the stock and bond markets. So, where will interest rates go from here?Well, it depends. There are 2 likely scenarios for the economy right now; the first being near-term volatility, followed by structural stagflation, the 2nd, disinflation, followed by possible deflation.

- The most likely near-term scenario is a period of market volatility followed by structural stagflation. This scenario is actually frightening. With the underlying weakness in the economy as a backdrop, oxygen-sucking major economic news dominates the headlines in the form of trade deal announcements, possible interest rate cuts, all fueling markets and creating buzz, and artificial stimulation. Laced in between, are some very bad news reports about layoffs, bankruptcies, and consumer distress. Whether the markets ultimately “shrug off” or react negatively to these reports largely depends on whom people listen to, and this is key. However, the inflationary effects of the tariffs and resulting supply shortages will be giving core inflation a boost. Partly offset by lower energy costs, they will probably get a huge shot in the arm from the new tax bill. Depending on how many short term stimulative gimmicks there are in the final bill, there will be some initial market euphoria as trillions in tax goodies will be handed out. This will be somewhat inflationary. A big reason why Powell is holding back on rate decisions is, he would like to see the final bill first. Why would he risk making a decision that could be muted by the effects of the tax bill? No matter what happens then, he would get the blame.

4. The second most likely near-term scenario is that markets react negatively to the negative economic news, the tariff negotiations fool no one, and massive layoffs start happening very quickly. We’ve already seen Mc Donald’s same-store sales drop off a cliff (a very good indicator), and there’s a lot of other widespread stress signals going on throughout the US economy. This weakness fuels rapid disinflation and possible deflation. The silver lining in this scenario is that Powell then drops interest rates, seeing no real impediments to doing so, and the economy gets another short-to-medium term stimulus effect, as consumers, businesses, and government are allowed to refinance debt at lower interest rates. This is probably the better of both scenarios EXCEPT…

The $37 Trillion Elephant in the room is the debt crisis.

5. Through any scenario, the debt crisis has not gone away. DOGE is a dud, and the prospect of massive cuts to social security and Medicare seem less and less likely as Mr. Trump fumbled away tons of political capital with his botched tariff rollout and various political wars he’s waging. This means high budget deficits are here to stay, and regardless of how low the interest rates go, the interest on the debt will be punishing. It will only be a matter of time before bond markets step in again, and start flexing their powerful muscles.

6. Caveats: Supply shocks, wars, pandemics, major disasters can all alter or forestall any of these scenarios. The most powerful evidence of that was the COVID pandemic. A war in the South China Sea or Iran would have major repercussions for markets, economies and political machinations throughout the world, and we must hedge accordingly.