After having predicted strong inflation far before most world-renowned economists, and after being similarly ahead of most others in instantly swatting down Jerome Powell and Janet Yellen’s views that inflation was transitory, we’re going to take a deep dive into what’s steering the US economy right now, and more importantly, where it’s going.

With the latest US inflation data in and running at a white-hot 8.6%, the answer to the question is a strong YES, as the Federal Reserve will be frightened into beaching the giant ship that is the US economy. Runaway inflation is a deep and valid concern, and interest rates is only one way to try and tackle the problem. The other ways to tackle the problem largely depend on consumer behavior, which will inevitably take a hit due to the cascade of bad news coming out about the economy.

Prior to the inflation announcement today, there was some hope that the Fed could “thread the needle” and escape a recession. Even here at REconomixTM we were slightly hopeful of such a scenario. Now that inflation has become very entrenched, the Fed must try its best to slow down the economy.

Structural Problems

As we all know, the Fed “printed” money for more then a decade, and the supply of money grew so large, it created asset bubbles. This is because in capitalism, money likes to go where it’s “taken care of,” and it likes higher returns. The result was asset bubbles in stocks, real estate, and cryptocurrencies, amongst others, which are being deflated by the promise of ever higher returns in safer assets, along with the slowing of demand in loans from banks. People tend to take out smaller loans, or none at all, when the cost to pay them back goes up.

The US economy is very exposed to the rest of the world because of the amount of free trade deals, exports, imports, and the amount of multinational corporations bringing profits or losses back home. The post-pandemic world saw a stimulus from central banks around the world, which means that money supplies increased, ultimately causing consumers around the globe to purchase more goods and services.

India and China are massive economies with growth trajectories which cause a rise in consumption of food, and other commodities around the world. In fact, if it weren’t for the state-mandated lockdowns in China, the global inflation problem would actually be worse!

Fiscal Policy

In the past 2 decades, the US government, as the “spender of last resort,” has propped up the flagging economy through running large budget deficits. This started with the Bush administration post 9/11, and increased during the Obama, Trump, and now Biden administrations. Much of the spending has been focused on defense and national security. In the course of the last 2 decades, defense and homeland security spending has been profligate at times. As one example, an entire fleet of new ships, called Littoral class destroyers, was created at a cost of several billion dollars. They are now rendered impractical and vulnerable, and are slated to be scrapped or sold off.

Energy

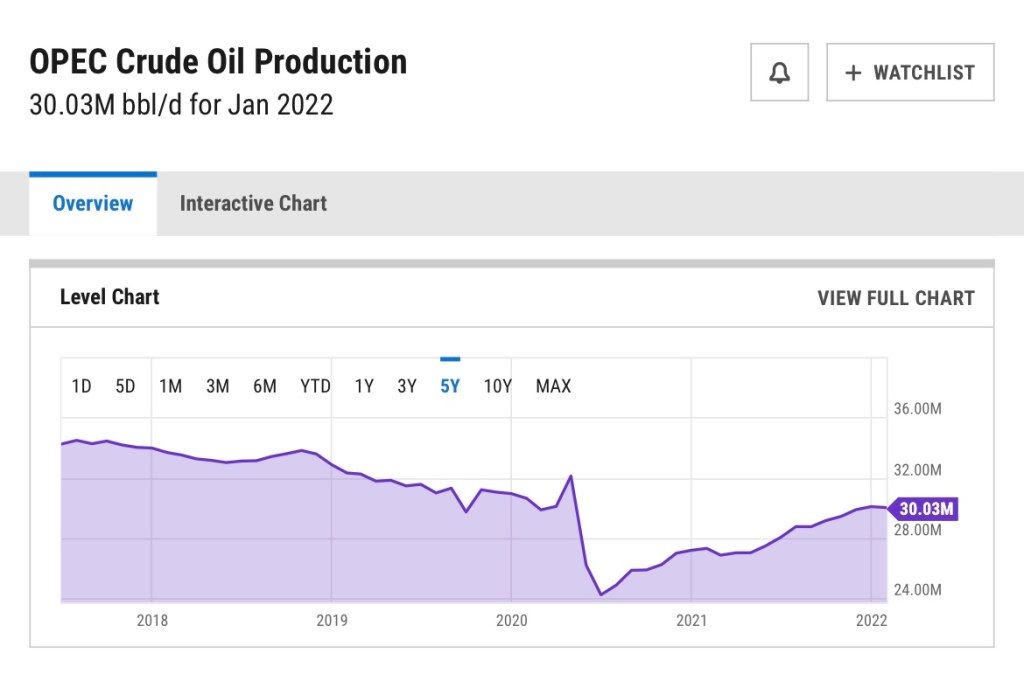

During the pandemic, the price to drill and transport oil got so low, it cost more to ship it and drill for it than it was worth. The demand for oil was extremely low compared to the supply. Large oil-producing countries, especially OPEC, decided that they would put limits on the production of oil to try to boost the price. Since the boom in global demand from people getting back to work, those production cuts are still in place.

Russia’s invasion of Ukraine resulted in sanctions of Russian oil and gas, which removed millions of barrels of oil a day at a time when we needed it most. To date, OPEC has not made any meaningful production increases to offset Russian oil. OPEC seems to be cashing in and making up for any losses from the pandemic.

Food

Food is a core necessity, like energy, and the prices of food are affected by energy. It takes energy to produce food products, refrigerate them, and transport them to stores. Agriculture has been affected by the rise in trade and incomes in China, as well as 3rd world countries, notably India, Africa, the middle east, Central and South America, and southeast Asia. As incomes rise, people tend to consume more food, and unfortunately, waste more food.

Other commodities

As the world increases in affluence and wealth, (especially India and China, which combined, have 2/5 of the world’s total population) commodities become more scarce during economic expansions. This includes metals, precious metals, and other goods.

Supply Chain Breakdowns

Post-pandemic, the supply chain disruptions were rightfully blamed for much of the rise in prices due to spot shortages of goods and commodities. It was relatively easy to return to work in the service sector, but the manufacturing and shipment of goods and commodities was greatly affected. This will be less of a factor over time, but many shortages remain.

The Perfect Storm

In conclusion, the aforementioned factors, and others have created a perfect storm of uncertainty, scarcity, war, fiscal irresponsibility, and irrational exuberance. The coming recession must be handled carefully by those in charge, as to not cause panic or severe disruptions and further scarcity in necessities. If the past is any indication, we are headed for political upheaval and widespread dissatisfaction with the status quo.